You delivered the goods. You did the work. The invoice went out — and then the waiting began. Sixty days later, you're still watching your cash flow bleed while your buyer's accounts payable team sends automated "processing" replies. This is the everyday reality for millions of SMEs. It doesn't have to be.

Invoice financing isn't a new concept—banks have been advancing cash against receivables for decades. The problem is the machinery behind it: manual document checks, multi-party credit assessments, correspondent banking delays, and a high risk of duplicate or fraudulent financing. According to Deloitte, processing a single trade finance transaction can take up to 10 days—before any money moves.

For an SME with tight working capital, that wait isn't a minor inconvenience. It's the difference between making payroll and missing it. As explored in Spydra's deep dive on supply chain finance liquidity gaps, this structural dysfunction is not a bug—it's baked into a system designed around large incumbents, not agile suppliers.

The IFC estimates the global trade finance gap exceeds $1.7 trillion—with SMEs accounting for the vast majority of unmet demand.

Tokenization converts a real-world financial asset—your invoice—into a blockchain-based digital token. That token is a verified, tamper-proof representation of your payment right. It can be financed, transferred, or settled without the paperwork carousel that bogsdown traditional processes.

As Spydra breaks down in its primer on tokenization in banking, this shift does more than speed things up—it fundamentally changes who can participate in financing your invoice. Instead of one bank gatekeeping access to capital, tokenized invoices can be funded bya broader network of institutional liquidity providers in fractional amounts, each taking a piece of the risk.

On permissioned blockchains like Hyperledger Fabric, this happens with full data privacy—commercial invoice details stay off the public ledger while the settlement logic is enforced by code.

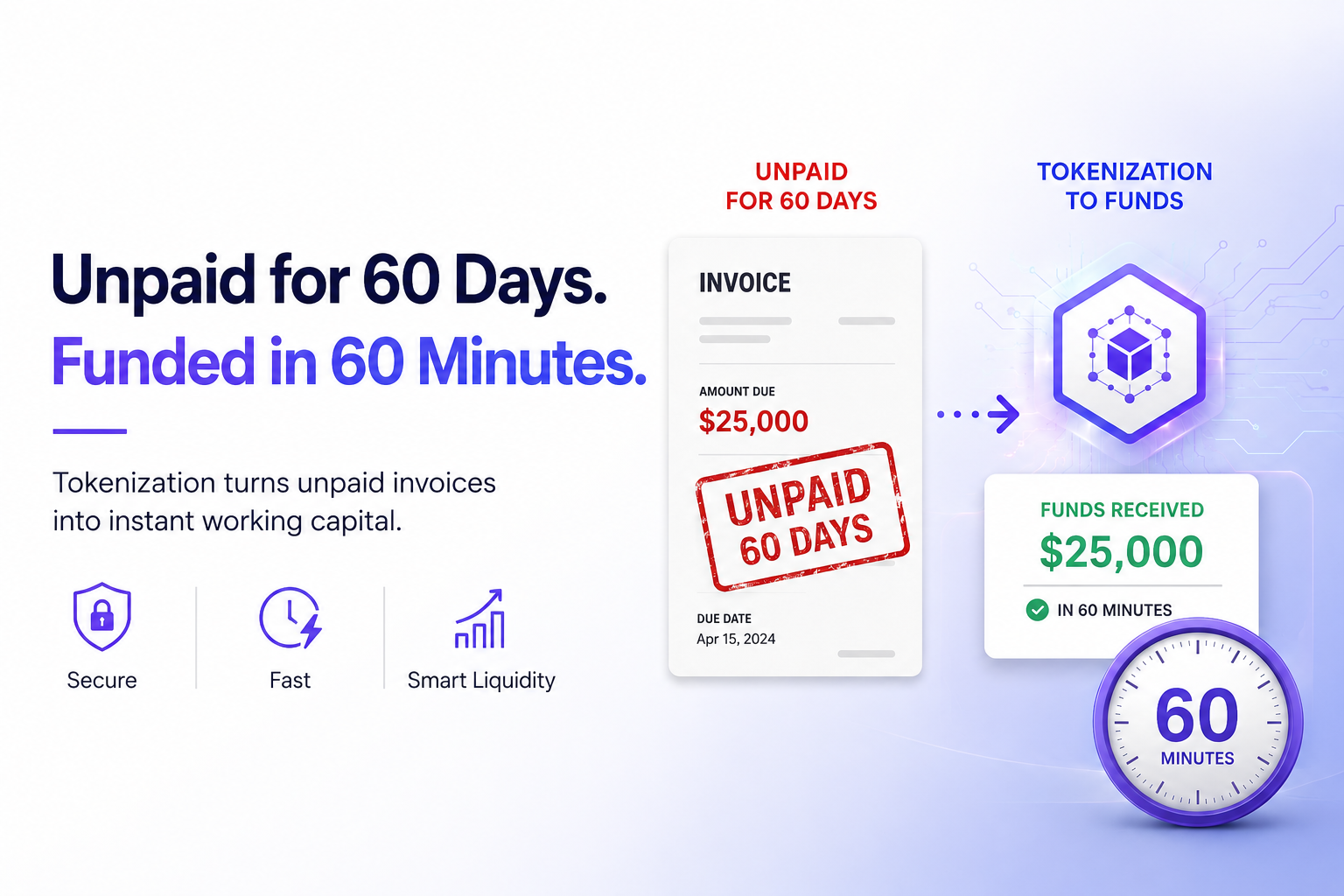

1. Invoice is issued and verified on-chain

Your invoice is submitted to the blockchain platform. KYC checks, buyer reputation, and invoice authenticity are verified automatically—no manual back-and-forth with an underwriter.

2. Invoice is tokenized as a digital asset

The verified invoice is minted as a blockchain token representing a verified payment right. This token is the asset that enters the financing marketplace.

3. Institutional liquidity providers purchase fractional portions

Institutional liquidity providers fund your tokenized receivable—at a discount—providing you with immediate working capital. Risk is distributed; your invoice doesn't depend on one institution's appetite.

4. Smart contracts lock and release capital

A smart contract holds the capital and automatically triggers settlement the moment the buyer's payment is confirmed—no manual reconciliation, no chasing.

5. You receive working capital—fast.

Instead of waiting 60–90 days, funds are accessible within hours. Enterprise pilots of tokenized receivable financing have demonstrated that manufacturers can receive working capital in 24 hours rather than weeks or months.

The infrastructure for tokenized invoice finance is live and already being used at scale.

As detailed in Spydra's overview of blockchain-powered tokenization in trade finance, institutions ranging from exporters to global banks are replacing legacy letters of lading with programmable liquidity cycles built on distributed ledgers.

The blockchain supply chain financing model—where tokenized receivables are financed against real-time buyer data with automated early-payment discounting—is already proving superior to traditional supply chain finance (SCF) in both speed and risk management.

BCG estimates that asset tokenization could unlock up to $4 trillion in new financing opportunities. A meaningful portion of that value lies in receivables that currently remain unpaid, draining working capital from businesses that have already earned it.

Spydra's dedicated supply chain finance solution is built specifically for this workflow, enabling enterprises to deploy invoice tokenization on Hyperledger Fabric without requiring deep technical expertise. Integration with the OCEN framework further streamlines supplier credit access for qualifying businesses.

If your buyers pay on 60- or 90-day terms and you're bridging that gap through a credit line or a factoring arrangement that charges 3–5% per transaction, tokenized invoice financing deserves serious consideration.

The benefits compound over time: faster access to capital enables quicker reinvestment, lowers financing costs, and helps prevent supply chain disruptions caused by delayed payments.

More importantly, tokenization reduces dependence on a single institution's risk appetite. When an invoice can be financed by a vetted network of institutional liquidity providers—automatically, transparently, and according to terms encoded in smart contracts—you are no longer dependent on a loan officer's spreadsheet.

The question is no longer whether this technology works. The question is whether your business is ready to stop treating unpaid invoices as unavoidable overhead and start treating them as the liquid assets they truly are.

Captures high-impression queries from readers who are familiar with factoring but new to blockchain-based alternatives.

Directly addresses the public-versus-permissioned blockchain confusion that the blog highlights. It is also valuable for featured snippet targeting.

Mirrors the blog's core value proposition ("60 minutes") and aligns well with voice-search and zero-click queries.

A practical concern that the blog does not fully address. Answering it helps build trust and overcome common objections.

Another important operational question SMEs are likely to ask before adopting the solution. It also helps differentiate Spydra's workflow from traditional supply chain finance (SCF), which often requires buyer onboarding.

Targets the "blockchain data privacy" query cluster, which is highly relevant to enterprise buyers concerned about confidentiality and compliance.

Aligns directly with Spydra's integration capabilities, including REST APIs, SAP, and other enterprise systems. This is a common pre-sales question from enterprise buyers.

One of the most common concerns among finance, legal, and compliance teams. Addressing this question positions Spydra as a credible, compliance-focused provider and helps reduce adoption barriers.