.jpg)

The way we hold and move money is evolving faster than ever. As digital finance reshapes global banking, deposit tokenization has emerged as one of the most transformative innovations in recent years. It allows banks to convert traditional deposits into secure digital tokens that operate on blockchain networks. These tokenized deposits retain the stability and trust of regulated banking while adding the speed, transparency, and programmability of digital assets. For financial institutions, regulators, and enterprises alike, deposit tokenization represents the next big leap toward a faster, smarter, and more connected financial ecosystem.

By doing so, institutions open new possibilities: real-time settlement, programmable money, reduced friction across rails, and tighter integration with decentralized financial systems. In this blog, we will:

Let’s dive in.

Deposit tokenization is the process of representing a bank deposit (i.e. fiat currency held at a regulated financial institution) as a digital token on a blockchain or permissioned ledger. Each token has a 1:1 backing by the underlying deposit. In other words, when you deposit $1,000 in a bank, the bank might issue 1,000 tokens representing that claim on your fiat deposit.

These tokens behave like money, but with programmable, blockchain-native qualities.

To situate deposit tokens among related concepts:

While deposit tokens are not necessarily legal tender, they allow commercial banks to offer on-chain money that is fully backed by deposits. As KPMG notes, tokenized deposits serve as a bridge between traditional banking and the digital economy. KPMG

Oliver Wyman also emphasizes that bank deposits already make up over 90 % of money in use today, and tokenizing them allows them to move into blockchain environments. oliverwyman.com

Hence, deposit tokenization complements—but does not entirely replace—stablecoins or CBDCs.

Deposit tokenization holds several potential advantages. Below, we explore each in turn, showing how they can reshape finance.

Traditional bank transfers (especially cross-border) often rely on legacy rails, clearing houses, and batch settlement. Tokenized deposits can settle instantly, literally peer-to-peer, in real time—and at any hour (24/7). This speeds up liquidity and reduces settlement risk.

Because deposit tokens reside on a programmable ledger, banks or users can embed logic via smart contracts:

This opens up new service models where deposits become not just static balances, but active financial tools.

By reducing intermediaries and reconciliations, tokenization can lower operational costs. Settlement layers, reconciliation systems, and manual accounting can shrink. Some manual processes and interbank intermediaries may get bypassed.

Tokenized deposits can travel across various blockchain networks, DeFi platforms (in permissioned settings), and financial infrastructures. Thus, deposit money becomes a “universal rail” within regulated environments.

With blockchain as the ledger, transaction histories become transparent (to permitted parties) and auditable. That helps with compliance and reduces fraud possibilities.

Because settlement is atomic (i.e. update ledger state in one transaction), there’s less risk of one party defaulting mid-process.

Banks can monetize the infrastructure, provide value-added services (e.g. programmable APIs, liquidity provisioning, token custody), and reduce reliance purely on interest income.

JPMorgan launched JPM Coin as an internal payment rail. Though limited to institutional clients, it shows how deposit-like tokens can speed settlement within a banking ecosystem. McKinsey & Company+1

Institutions can use deposit tokens in cross-border settlement, as collateral in securities trades, margin in derivatives, or for intra-bank cash pooling.

Corporate treasuries may use tokenized deposits to connect with lending platforms, tokenized asset markets, or cash management protocols in a regulated environment.

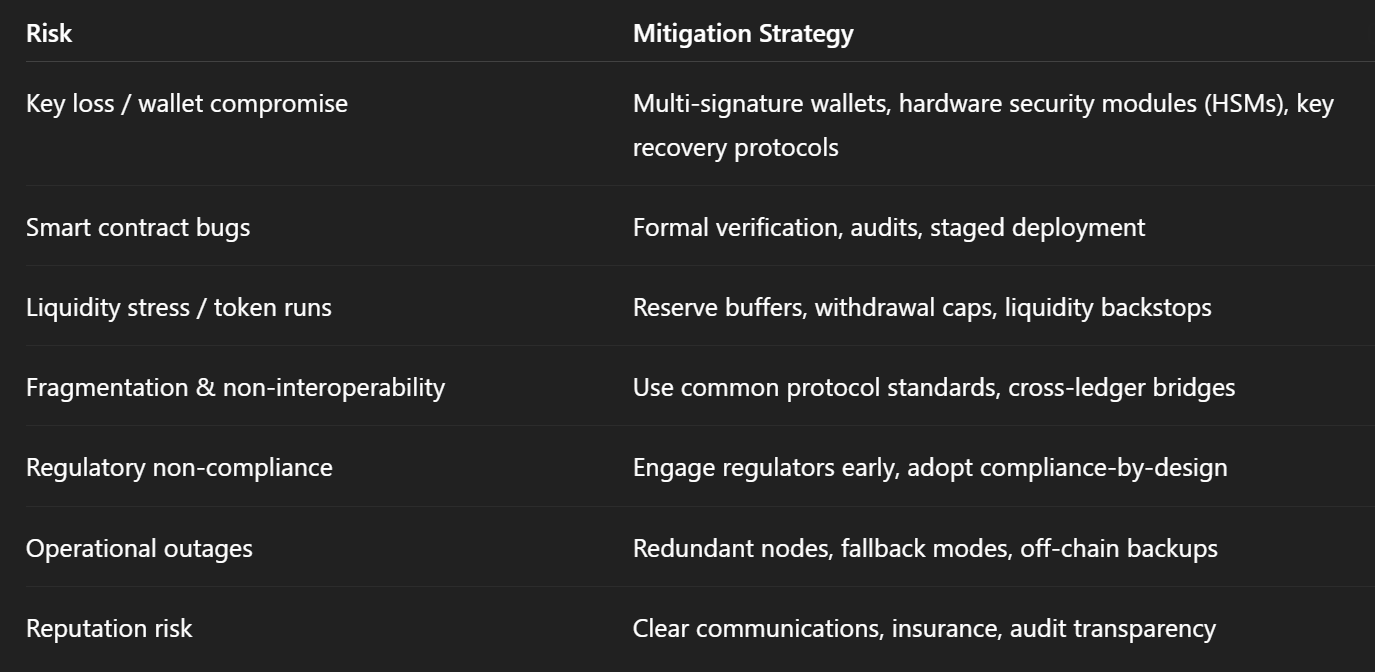

While exciting, deposit tokenization faces hurdles. It must navigate operational, regulatory, and technical challenges. Below are key risks.

Tokenization may run into constraints in existing banking, securities, or payments regulation. Who bears liability if a token is hacked? Are tokens legal contracts? Regulators must clarify custody, settlement finality, and consumer protection.

The EBA’s report underscores the need to monitor tokenization and ensure it fits into financial stability frameworks. eba.europa.eu

Digital tokens depend on cryptographic keys. If keys are compromised or lost, access to deposits may be lost. Banks must ensure secure custody, redundancy, key recovery, and wallet security.

Different banks and platforms might adopt different protocols or chains. Without standards, fragmentation risks arise.

Users may demand redemption from tokens to fiat. The underlying system must guarantee liquidity and seamless conversion between token and deposit forms.

Nodes, smart contract bugs, ledger software errors, and network outages may jeopardize service.

If many depositors move into tokenized lanes, traditional banks might lose funding stability or face “runs” within the token ecosystem.

Balancing transparency with user privacy is nonstop. Financial systems need to hide sensitive data while providing auditability for regulators.

In order to ground this discussion, let’s look at some real-world data on bank deposits, tokenization trends, and digital money momentum.

These numbers show that deposits remain a huge financial base—thus, tokenizing even a fraction would represent a sizeable opportunity.

These trends suggest strong institutional appetite for digital forms of money beyond central banks.

Here’s a simplified architecture and flow for deposit tokenization in a regulated banking environment:

Because the deposit tokens always correspond 1:1 to real deposits, this architecture preserves the safety of fiat deposits while layering digital rails above them.

Banks or financial institutions considering deposit tokenization can follow these steps:

Start with an internal or limited customer pilot. Use a permissioned blockchain (e.g. Hyperledger, Corda, or Quorum). Focus on internal settlements, between branches or subsidiary operations.

Form a consortium of banks or clearing institutions. Enable tokenized deposit transfers between banks, clearing houses, or settlement systems. Implement shared standards.

Expose APIs so corporate clients, fintechs, or treasuries can mint, transfer, and redeem deposit tokens. Add programmable features (interest, escrow, conditional payments).

Integrate deposit tokens as collateral or liquidity in tokenized securities markets, DeFi-like protocols (in regulated settings), or token-based lending.

Scale to many users, integrate with foreign banks, cross-border rails, and hybrid CBDC–commercial bank systems.

At each phase, maintain regulatory compliance, risk controls, and robust operational resilience.

Regulators must treat deposit tokens carefully. Key areas to address:

Several regulators (e.g. the EBA) are already drafting frameworks and monitoring tokenized deposit projects. eba.europa.eu

In India, RBI’s pilot program will help regulators understand how deposit tokenization can align with existing monetary and banking laws. Reuters+1

To succeed, stakeholders must manage certain risks:

Continuous monitoring, stress testing, and governance are critical.

If deposit tokenization becomes mainstream, banks will evolve into infrastructures: issuing, custody, settlement, and service providers for tokenized money.

Deposit tokens could capture flows that currently go to stablecoins. Standard Chartered estimates stablecoins could draw $1 trillion from emerging market bank deposits over the next three years. Reuters

However, for regulated environments, deposit tokens may offer more confidence and oversight than private stablecoins.

Tokenization likely starts in wholesale, interbank, and institutional realms before moving to retail. Over time, core deposit pools may be gradually tokenized.

Tokenized deposits may make cross-border capital flows more efficient, blurring lines between domestic and global liquidity. As BIS data shows, cross-border banking claims continue to evolve at large scale ($629 billion expansion in Q3 2024). bis.org+1

If implemented thoughtfully, deposit tokenization can unlock faster, more programmable finance while preserving the safety of regulated banking.

1. What is the difference between deposit tokenization and stablecoins?

Deposit tokenization issues tokens by regulated banks, backed 1:1 by deposits. Stablecoins are generally privately issued tokens backed by reserves. Deposit tokens aim to retain regulatory oversight and banking safeguards.

2. Can I redeem deposit tokens for fiat currency?

Yes. Users must always have the right to redeem tokens for the equivalent fiat deposit (i.e., burn tokens, receive cash).

3. Are deposit tokens legal tender?

Not necessarily. Unless declared by a central authority, tokens are not legal tender. But they represent valid contractual claims on deposits under law.

4. Which blockchain makes sense for deposit tokens?

Permissioned blockchains (Hyperledger, Corda, Quorum) or regulated ledgers often make sense initially due to compliance needs.

5. Can tokens cross between different blockchains?

Yes, via cross-chain bridges or interoperability protocols—but they must ensure atomicity and maintain backing integrity.

6. What happens if a private key is lost?

That user loses access to their tokens. Banks must implement key recovery, multi-signature, or custodial safeguards.

7. Will depositors face additional fees or costs?

Banks may charge token transaction fees similarly to payment rails. However, cost savings from efficiency may offset that.

8. Do deposit tokens affect bank liquidity or stability?

Potentially. If many depositors shift to tokenized channels, banks must ensure funding stability and run protections.

9. How do regulators supervise tokenized deposits?

They’ll monitor for AML/KYC compliance, liquidity buffers, audit trails, consumer protection, and financial stability metrics.

10. Are deposit tokens vulnerable to hacking?

Yes, as with any digital asset. Security, audits, and operational robustness must mitigate this.

11. Will deposit tokenization replace traditional banking?

Unlikely. Rather, it complements banking by layering digital rails above fiat deposits.

12. When will deposit tokenization become mainstream?

Mainstream adoption may take years. But pilots, wholesale systems, and institutional use could emerge within 2–5 years.

13. How do depositors trust that tokens remain backed by deposits?

Banks should provide audited reserves, real-time proofs, and transparency, possibly via cryptographic proofs or audits.

14. Can deposit tokens be used cross-border?

Yes—subject to regulatory, legal, and interoperability constraints—making cross-border settlement more efficient.

15. How do deposit tokens compare with CBDCs?

CBDCs are central bank–issued and represent legal tender. Deposit tokens are issued by banks and represent claims on those banks’ fiat deposits. They serve complementary roles.